My name is pronounced as if you’re sneezing —— ‘Hǎi Qín!’

I am a Research Consultant in the World Bank’s East Asia and Pacific Chief Economist Office in Washington, D.C. I earned my Ph.D. in Economics from Fudan University in March 2026. I received my B.A. in Mathematical Economics from Fudan in 2021, with a second major in Data Science.

Research fields

Primary: International Finance & Macroeconomics; Secondary: Uncertainty

I research nonlinear interactions between international policy regimes and multidimensional monetary policy spillovers.

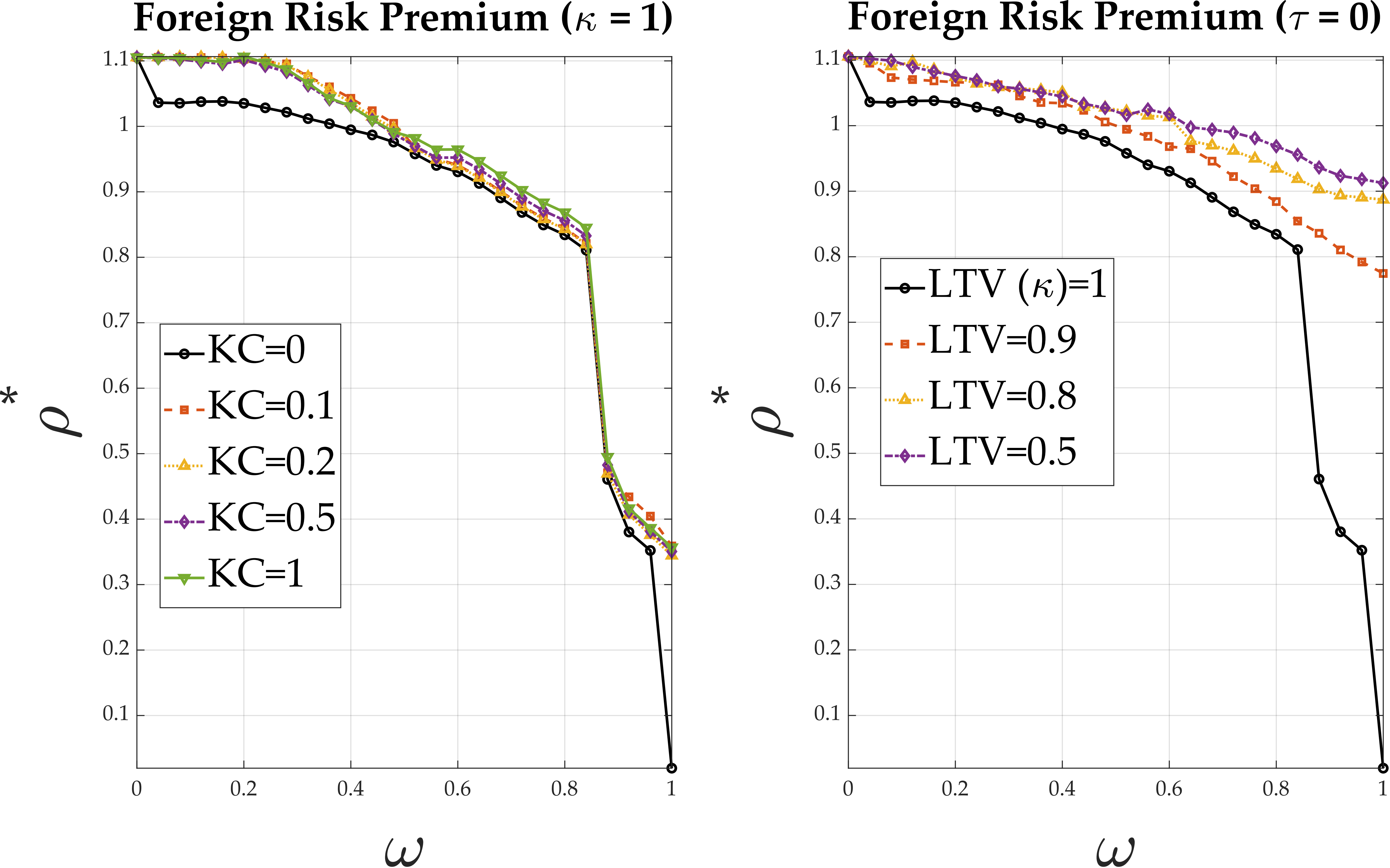

Numerical examples from a two-country monetary model with collateral constraints show that macroprudential policy is a more robust buffer than capital controls:

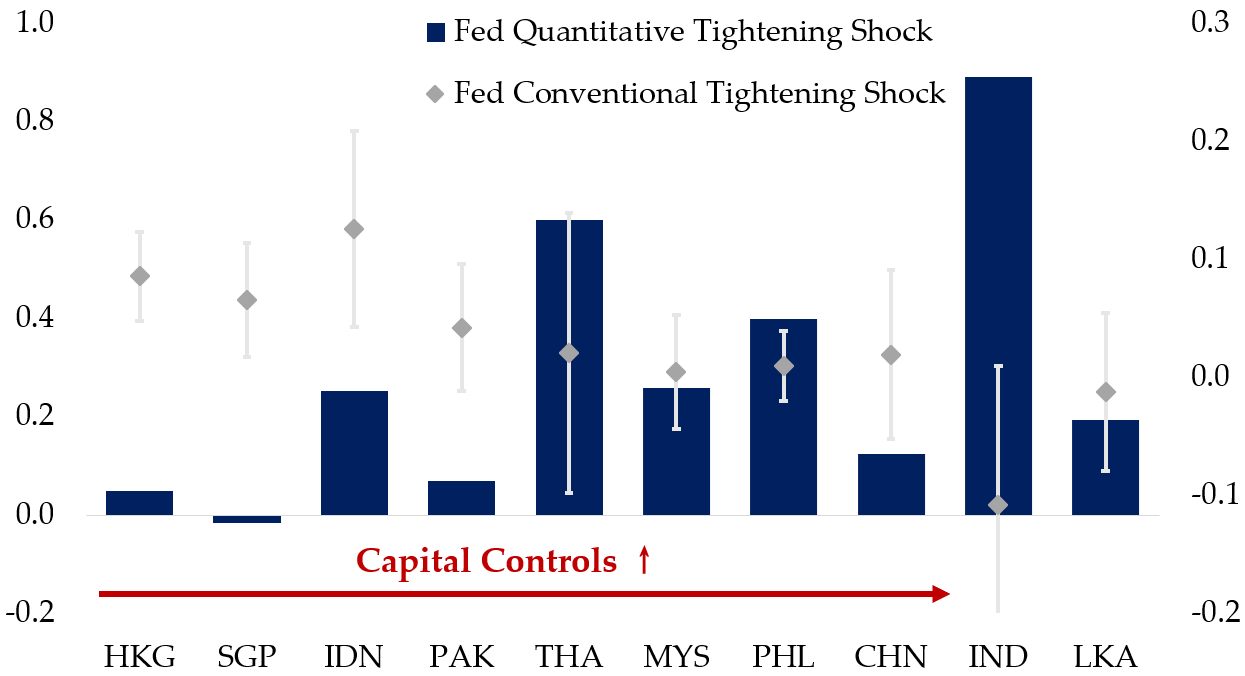

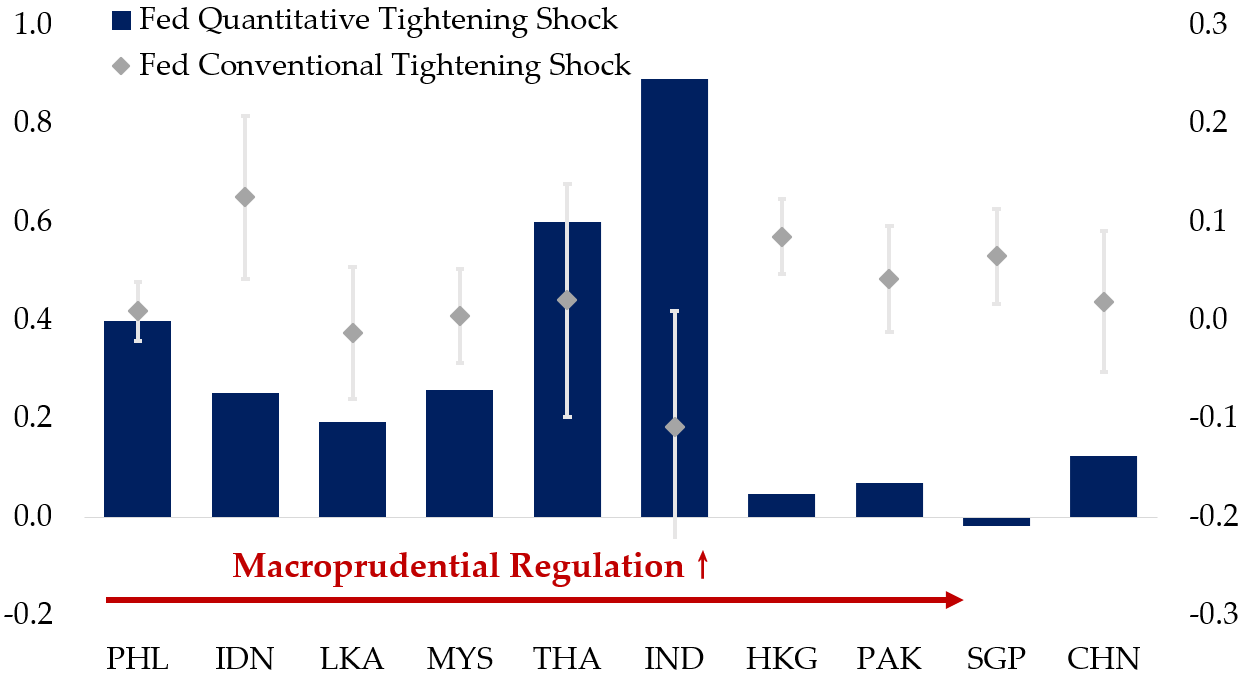

Representative examples from Asian economies: \(\Delta \ln({\rm Spread})_{c,s,\tau}=\textcolor{magenta}{\boldsymbol{\beta}^c_1}\,u_{1,\tau} + \textcolor{blue}{\boldsymbol{\beta}^c_2}\,u_{3,\tau} + \alpha^c_s+\varepsilon_{c,s,\tau}. \text{ EMBI spread; CDS for HKG and SGP.}\)

* MPru stance is measured as the cumulative sum of the MPru action indicator.